How to Know if You Want to Be an Auditor

It is a misconception that the responsibilities of an external accountant can be summed up to individuals that examine financial records with the goal of forming an opinion about the fairness of information presented within a visitor's fiscal statements. An inspect, in a broader sense, is a method of creating an opinion or conclusion well-nigh processes, transactions, or other information when compared to a standard or criteria. There are a variety of dissimilar services or reasons a company may need to appoint an auditor.

If embraced, business owners can use auditors as tools to enhance processes and procedures, create a tone from the superlative that deters fraudulent activity, and hold both management and employees accountable to execute their roles and responsibilities. In this post, we will review a number of topics to proceeds an understanding of an auditor's responsibilities in completing an audit and the professional person duties they hold equally an external auditor.

What are the Main Functions of an Accountant?

Below are examples of dissimilar audit functions, the auditor's duties, and scope of piece of work:

Internal Audit

An internal auditor is responsible for performing procedures that test the efficiency and effectiveness of company internal controls put in place to attain business organization objectives. The scope of an internal inspect includes all financial and operational controls that are used to create maximum productivity at a company. Example findings or duties include:

- Provide recommendations to improve weak internal controls

- Investigate instances of possible fraud (even those considered immaterial)

- Perform reconciliations of fiscal and operating data

- Monitor compliance with industry standards, laws, and guidelines

- Evaluate whether processes and procedures are functioning properly

Forensic Audit

An auditor is responsible for using a mixture of audit and investigative techniques to determine whether the suspicion of fraud is warranted and if so, the effects of the fraud. The scope of forensic audits can be as wide equally necessary and can have a significant amount of time and resources. Generally, a successful forensic audit relies greatly on the types of monitoring a visitor has in identify. This allows a forensic auditor to employ logs and information captured as part of monitoring to put an authentic timeline together.

Attestation Services

An external accountant is responsible for providing different services to clients such as guidance on accounting-related matters, technical disciplines, or industry cognition. Scope of work depends on services rendered simply is generally divers by an understanding betwixt the customer and auditor.

Auditors study on subject matters similar the blueprint and operating effectiveness of a service arrangement's internal controls over a certain objective such every bit security. This is too known as Arrangement and Organization Controls (SOC) Reports. Encounter below for more than data on this type of written report.

Information System Audit: Sample Attestation Service

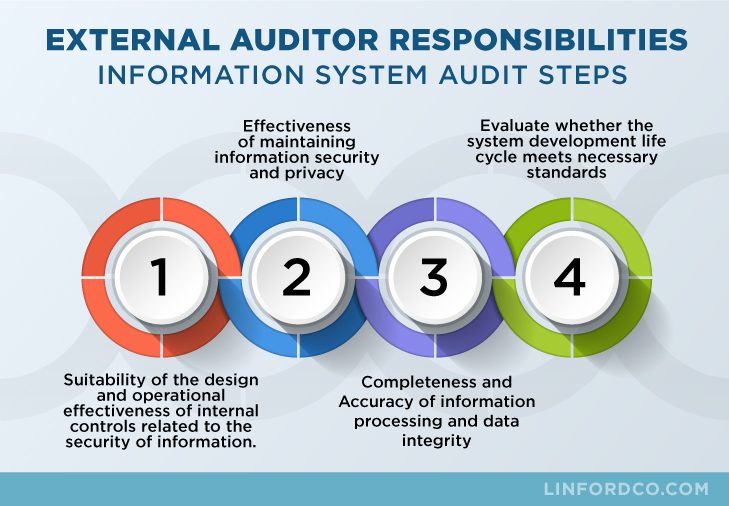

An external accountant is responsible for evaluating the internal controls pertinent to a company'southward It infrastructure. Scope of information organization audits tin can be determined based on a specific objective only generally include the following steps.

- Suitability of the design and operational effectiveness of internal controls related to the security of information. Types of internal controls include logical and physical access, information transmission, and organization health monitoring. See more than nearly specifics related to SOC reports at some of our other posts here, such every bit "What is a SOC 1 Report?"

- Effectiveness of maintaining information security and privacy

- Completeness and Accuracy of data processing and data integrity

- Evaluate whether the organisation development life bicycle meets necessary standards

What are the Duties and Responsibilities of an External Auditor?

The AICPA has defined the professional person responsibilities of auditors performing testament services. As outlined in AU Department 110, an accountant's responsibilities when performing a fiscal statement audit is to create a programme so execute that programme past collecting applicable supporting show to brand a determination, or opinion, on whether or not the financial statements presented by management are free and articulate of whatsoever material misstatements that were presented by way of error or fraudulent activity. Whatsoever errors or fraud that practice non meet the threshold for materiality are not the responsibility of the auditor

For other types of attestation examinations, auditors are responsible for following SSAE 18. SSAE 18 details an accountant's responsibilities in performing an audit, and reporting on the opinion, conclusion, or findings in accordance with the testament standards and type of engagement. While an external auditor is responsible for making sure that the opinion, findings, or conclusion are reported in accord with requirements, the ultimate responsibleness of the field of study thing itself is still the responsibility of the client. Let's talk a little more nigh that.

Another responsibility of an auditor includes the request for direction to supply a written and signed assertion. Why is an assertion then of import you may inquire? The elementary respond is that auditors base their stance, conclusion, or findings on the information provided by management. Considering of this, management is responsible for explicitly stating to the users of their inspect report that the data within the report is consummate and authentic. This is all outlined as function of the assertion. If management will non provide this assertion, an auditor will be required to provide a modified opinion.

What Skills Do Auditors Demand?

Auditors are required to retain the type of skills such as proper education, industry background, and working knowledge when acting as an external auditor nether SSAE 18. Having the right type of expertise is particularly essential because auditors are oftentimes required to exercise their own professional sentence in determining whether certain criteria are met or if an stance should exist qualified. In addition to having the correct type of proficiency, external auditors are also expected to follow certain ideals requirements. These requirements are outlined in the AICPA's Application Code of Professionalism.

Depending on the type of audit or testament appointment underway, the blazon of designations required will probable differ. A skilful place to outset is at CPA firms. If your arrangement requires an attestation date, the report will only be legitimate if it is signed by a CPA or CPA firm.

This is, all the same, but the beginning. Attestation services tin can include a number of different processes from fiscal services, it services, cryptocurrency, oil and gas, health intendance and the list goes on. When engaging an external auditor to perform these services, doing the proper due diligence such as checking designations such as CISSP, CISA, or past references should be reviewed to determine whether those working on the appointment have the correct type of background.

Why are Auditing and the Auditor Important?

Many times, people cringe at the sight of auditors, but it is important to understand what auditors do and their office in creating a better business organization. Auditors provide the opportunity for business organisation owners to incorporate independence into the review process of their internal control programme. Additionally, the procedure helps to define gaps, weak controls, and possible risks. Moreover, recognizing the dissimilar functions auditors can provide, and using their services as an asset, can ultimately provide companies with an edge over their competitors.

Do Auditors Get Audited?

In fact, yes, auditors practice get audited past a third-party auditor. This is done as a way to determine whether a CPA house and the individuals working there have the correct technical knowledge and that processes are in place to follow planning and reporting requirements. The AICPA Peer Review Plan is completed once every three years.

Summarizing the Accountant Responsibilities and Duties

Hopefully, every bit yous read through this mail, it became clear that choosing the correct auditor for the type of engagement your organization needs is extremely of import. The responsibilities of auditor and client are truly maximized when both parties understand their roles in the audit process. As a summary, those external accountant responsibilities include the following:

CPA Firm will be conducting the audit

- CPA Firm staff working on the audit take the necessary skills to provide professional judgement

- CPA Firm has been through a peer review at least 1 fourth dimension in the final 3 years

- CPA Firm requires that direction provide a written assertion

- CPA Business firm acts in a professional person and ethical manner

These key concepts when picking an auditor should exist central as your organization decides on engaging an external auditor in the future.

If yous have any additional audit questions or concerns, or accept an upcoming audit engagement, and are in need of CPA services, please contact Linford & Co.

Jaclyn Finney started her career as an auditor in 2009. She started with Linford & Co., LLP. in 2016 and is a partner with the firm. She is a CISA with a special focus on SOC, HITRUST, FedRAMP and royalty examinations. Jaclyn works with her clients to provide a process that meets the needs of each customer and generates a tailored report that is useful to the client and the users of the report.

Source: https://linfordco.com/blog/understanding-auditor-responsibilities/

0 Response to "How to Know if You Want to Be an Auditor"

Post a Comment